- Do your application and interview processes comply with current human rights laws? It may sound surprising to hear that, but there are still some employers out there that just don't get it.

- If you use agencies to assist you in the selection process, do they actually check out beforehand the candidates they send out to you? Many do not, hoping that the "halo effect" gained during the interview process will cause employers to not insist on finishing off the process, but they have been successfully sued in the courts for failing to do so.

- Regardless of that, are you conducting reference checks for positions that would involve contact with the public? One company that ran a tavern failed to do that in hiring some bouncers. A customer who was then viciously attacked by them in the tavern's parking lot successfully sued the employer for failure to properly check out the bouncers' background beforehand (which would have immediately raised some red flags). That principle was subsequently upheld in another case at the Supreme Court of Canada.

- Are you being straightforward in describing the position and its prospects to the candidate, and does he reciprocate in describing his capabilities and achievements, as well as assuring that he would not be in breach of his employment contract with his current employer? Failure to do so may constitute negligent misrepresentation, as noted by the SCC in Queen v Cognos, or potential exposure to suits from the former employer for poaching in breach of contract or fiduciary duty.

- Given the emergence of the common law in the area of privacy rights, as well as statutory requirements for several provinces and at the federal level, are you getting prior written consent for contacting referees, and are you explaining beforehand the exact purpose for checking such references?

- Does the employment agreement meet, at minimum, the requirements of employment standards legislation in your jurisdiction, as well as plainly explaining the terms that exceed such requirements? Among areas that many employers take for granted are the entitlement to, and calculation of, vacation pay and overtime.

- Are you making sure that the employment agreement presented to the candidate has been reviewed by your lawyers, that there are no terms outside the agreement that have not been properly documented, that the candidate has had the opportunity to get independent legal advice, and that it is fully signed off before he/she begins work? All steps are extremely important in order to ensure the validity of what was intended.

07 February 2016

The hiring minefield these days

I've addressed this issue several times before, but the topic just seems to be covering a wider area over time. Here are some current notes:

03 February 2016

A social look at the Canadian profession

It's been interesting to see the heavy promotion CPA Canada has been giving lately for its brand, and fascinating to note that they are promoting a single image of what that is supposed to represent to employers. However, the legacies of the predecessor designations will last for a very long time.

It appears that very little work has been undertaken to examine the effects they have left on the profession. There was one very bad joke going around a while back to explain the differences:

But it's not that simple. The former professional bodies were created to serve different needs that arose as time went by:

The different modes of training also have had their effect: the "bullpens" the CA candidates were in while they got ready for the UFE created alumni networks that have helped them out greatly over the years, even if many of them adopted the white-shirt and navy-suit stereotype along the way. On the other hand, the CMAs and CGAs had to study on their own (sometimes even by correspondence), and have tended to treat the organizations they work for as being the focal point of their social interaction. The latter probably explains why many of them have tended to be introverted in broader settings.

The CMAs also had an influx of membership back in the 1970s and 1980s from the transfer over of British graduates of ICMA (the Institute of Cost and Management Accountants, now the Chartered Institute of Management Accountants), and their superiority complex tended to muddy things up for a while for the homegrown RIAs. However, that is a story that has never been properly explored. Thankfully, the ICMA influx has long since retired.

I generally found the RIAs to be the most sociable of the bunch (conflict of interest disclosure: I'm one of them myself), and more likely to want to go out and relax together over a drink after work. You really learned a lot listening to those fellows in such a setting, and that type of camaraderie has been lacking for a long time among the more recent graduates. Of course, it cost a lot more for the newer CMA grads for funding their tuition compared to what we faced, and the Board Report stage did force some social interaction to take place in order to achieve a goal, so it may not have been that bad. However, I have heard instances of many employers not reimbursing all of the costs involved, or of setting up tracks to assure the progression of such candidates to more deserving positions, as opposed to the CATO system the CAs had.

What will the new CPA graduates face, and what will be the consequences for those that have come before? Those questions are very much open, and it would be interesting to see if someone (most likely an academic) will step up and investigate this.

It appears that very little work has been undertaken to examine the effects they have left on the profession. There was one very bad joke going around a while back to explain the differences:

"CGAs do good books. CMAs explain what they mean. CAs bend them to fit GAAP."

But it's not that simple. The former professional bodies were created to serve different needs that arose as time went by:

- The Chartered Accountants (CAs) were the first to be formed, initially in Montreal (the Association of Accountants of Montreal), and then in Toronto (the Institute of Chartered Accountants of Ontario). The Toronto group appeared to be more aggressive in extending membership to people of various qualifications, and there was a breakaway movement that formed the Dominion Association of Chartered Accountants in order to raise standards and confer a uniform national designation. That caused a rift that only healed in 1910, with the ICAO being triumphant and the CA designation being conferred province by province. DACA would become the Canadian Institute of Chartered Accountants in the 1950s, and the qualification and reporting standards gradually became more uniform nationally with university degrees required before entry into their programme only in the 1960s.

- The Certified General Accountants (CGAs) began as a group to provide accounting training for employees of the Canadian Pacific Railway, and it branched out from there. There was a running battle going on for decades between them and the CAs as to the right to audit financial statements, and this was fought out both in the legislatures and the courts. Their final inclusion in CPA Canada is rightfully seen as a miracle of negotiation.

- The Certified Management Accountants were initially created by the CAs as a subgroup of their members to cover the growing field of cost accounting before the CGAs had a chance to get into it. It then started holding its own examinations to confer "certificates of efficiency" to newcomers, and then created the separate Registered Industrial and Cost Accountant (RIA) designation in the early 1940s. The RIAs became the CMAs in the mid-1980s, and that time they started to required the possession of a university degree before entry into their course of study.

- The Certified Public Accountants (the original CPAs) came about in the mid-1920s to professionalize the accountants and auditors that worked for the taxation authorities in Ottawa and Queen's Park. The designation originated as LA (Licentiate in Accountancy) during 1926-1931, changing to IPA (Incorporated Public Accountant) during 1931-1936, before becoming the CPA. They merged with the CAs in the early 1960s.

- There were also the Accredited Public Accountants (APAs) out West, which existed from 1950 to sometime in the 1970s before merging with the CGAs. I have no information as to the reason for their formation in the first place, but it does explain somewhat why the CGA membership tended to be more heavily weighted to the Western provinces.

The different modes of training also have had their effect: the "bullpens" the CA candidates were in while they got ready for the UFE created alumni networks that have helped them out greatly over the years, even if many of them adopted the white-shirt and navy-suit stereotype along the way. On the other hand, the CMAs and CGAs had to study on their own (sometimes even by correspondence), and have tended to treat the organizations they work for as being the focal point of their social interaction. The latter probably explains why many of them have tended to be introverted in broader settings.

The CMAs also had an influx of membership back in the 1970s and 1980s from the transfer over of British graduates of ICMA (the Institute of Cost and Management Accountants, now the Chartered Institute of Management Accountants), and their superiority complex tended to muddy things up for a while for the homegrown RIAs. However, that is a story that has never been properly explored. Thankfully, the ICMA influx has long since retired.

I generally found the RIAs to be the most sociable of the bunch (conflict of interest disclosure: I'm one of them myself), and more likely to want to go out and relax together over a drink after work. You really learned a lot listening to those fellows in such a setting, and that type of camaraderie has been lacking for a long time among the more recent graduates. Of course, it cost a lot more for the newer CMA grads for funding their tuition compared to what we faced, and the Board Report stage did force some social interaction to take place in order to achieve a goal, so it may not have been that bad. However, I have heard instances of many employers not reimbursing all of the costs involved, or of setting up tracks to assure the progression of such candidates to more deserving positions, as opposed to the CATO system the CAs had.

What will the new CPA graduates face, and what will be the consequences for those that have come before? Those questions are very much open, and it would be interesting to see if someone (most likely an academic) will step up and investigate this.

11 January 2016

What is a workforce worth?

When attempting to allocate fair values to assets upon acquisition of an enterprise, there is always a challenge when dealing with residual amounts to intangible assets, especially in distinguishing between those with finite lives as opposed to infinite ones. One argument I have encountered in several circumstances is how much of a valuation one can attach to an enterprise's workforce in contributing to enterprise value. Most of those instances have tended to be based on false assumptions, as a workforce can fundamentally change after a takeover, whether through turnover, planned reductions by the acquirer, or just overly optimistic estimations of the workforce's capabilities.

As far as financial reporting is concerned, IFRS has mostly ruled out such allocations to intangible assets of finite lives. IFRS 3 explicitly states that it is not an identifiable asset (at par. B37). In addition, IAS 38 points out that there is insufficient control over the economic benefits that may result from the assembled workforce (at par. 15). However, there are several identifiable assets that can arise in that area, such as non-competition agreements or employment contracts that are determined to be below-market from the employer's perspective. These, and especially the latter, would be quite sensitive information, in which the detail would be best kept locked away in the acquirer's files!

A valuation may still be relevant in determining allocations to intangible assets that are allowed to be recognized, such as a relationship with a key customer. In such an instance, it is seen as a contributory asset, a relevant part of which is there to sustain the relationship. The best method for determining its value is seen to be that of "reproduction cost" (as opposed to "replacement cost"), which would include the cost of recruiting, training and allowing for attaining maximum effectiveness after going through the appropriate learning curves. This is a component of what is known as the "multi-period excess earnings method," which is a fallback calculation when a more direct estimation of economic benefits is not possible. This is quite an arcane area which has still not been fully discussed in the professional literature, and I have never seen it being properly calculated in practice by others.

That is a summary explanation of the quantitative considerations involved in this matter. There is also the qualitative side, which is often given short shrift in M&A discussions. However, many acquisitions have failed spectacularly, because the acquirer failed to take note of what was happening under the surface at its target.

The corporate cultures of both parties, and potential clashes, is a particularly well-known area for potential downfalls. A target's corporate history, however, may be of more relevant interest. For example, the skills needed to handle startups are not necessary appropriate when the enterprise becomes more mature, and an owner-entrepreneur's behaviour is quite different from that of a professional manager. As well, personal relationships—on many levels, both inside and outside the enterprise—may influence future outcomes, both before and after an acquisition takes place, and those tend to be insufficiently documented. It may well be in an acquirer's best interest to buy some drinks at the bar for some of the key parties (not necessarily at the top levels) or third parties and have a wide-ranging chat with them, before any approaches are being considered. That would be money well spent, before intentions are actually expressed, non-disclosure agreements are signed, and people start feeling committed toward achieving an outcome that would not eventually be beneficial to the acquirer. Of course, there are some crucial legal aspects that are also involved in this entire process, so it might be a good idea to discuss your proposed tactics with a lawyer with great M&A experience before going ahead.

As far as financial reporting is concerned, IFRS has mostly ruled out such allocations to intangible assets of finite lives. IFRS 3 explicitly states that it is not an identifiable asset (at par. B37). In addition, IAS 38 points out that there is insufficient control over the economic benefits that may result from the assembled workforce (at par. 15). However, there are several identifiable assets that can arise in that area, such as non-competition agreements or employment contracts that are determined to be below-market from the employer's perspective. These, and especially the latter, would be quite sensitive information, in which the detail would be best kept locked away in the acquirer's files!

A valuation may still be relevant in determining allocations to intangible assets that are allowed to be recognized, such as a relationship with a key customer. In such an instance, it is seen as a contributory asset, a relevant part of which is there to sustain the relationship. The best method for determining its value is seen to be that of "reproduction cost" (as opposed to "replacement cost"), which would include the cost of recruiting, training and allowing for attaining maximum effectiveness after going through the appropriate learning curves. This is a component of what is known as the "multi-period excess earnings method," which is a fallback calculation when a more direct estimation of economic benefits is not possible. This is quite an arcane area which has still not been fully discussed in the professional literature, and I have never seen it being properly calculated in practice by others.

That is a summary explanation of the quantitative considerations involved in this matter. There is also the qualitative side, which is often given short shrift in M&A discussions. However, many acquisitions have failed spectacularly, because the acquirer failed to take note of what was happening under the surface at its target.

The corporate cultures of both parties, and potential clashes, is a particularly well-known area for potential downfalls. A target's corporate history, however, may be of more relevant interest. For example, the skills needed to handle startups are not necessary appropriate when the enterprise becomes more mature, and an owner-entrepreneur's behaviour is quite different from that of a professional manager. As well, personal relationships—on many levels, both inside and outside the enterprise—may influence future outcomes, both before and after an acquisition takes place, and those tend to be insufficiently documented. It may well be in an acquirer's best interest to buy some drinks at the bar for some of the key parties (not necessarily at the top levels) or third parties and have a wide-ranging chat with them, before any approaches are being considered. That would be money well spent, before intentions are actually expressed, non-disclosure agreements are signed, and people start feeling committed toward achieving an outcome that would not eventually be beneficial to the acquirer. Of course, there are some crucial legal aspects that are also involved in this entire process, so it might be a good idea to discuss your proposed tactics with a lawyer with great M&A experience before going ahead.

10 December 2015

Current considerations for appraising capital expenditures

As I was alluding to yesterday, the appraisal of capital expenditures has become much more complex since CMA Canada last explored the topic in 1981. Here are some aspects to consider:

Updates: Typo corrected; "process improvement" and "investment properties" added in investment categories; give examples of non-relevant financing issues.

- The greater participation of the public sector has called for different types of focus. While the cost of capital will tend towards the risk-free rate, there are also greater requirements for considering optimism bias and sensitivity analysis in different components of proposals, the allocation of risks that arise in public-private partnerships, and consideration of relevant benefits to society (including discussion of what is not relevant).

- In the private sector, more rigorous pre-acquisition analysis is required to determine which components are capital and which are expense, for both financial reporting and tax purposes. This is effectively a 2x2 grid, and there is very little summary literature on the topic.

- In the private sector, the after-tax cost of capital will need to be risk-adjusted depending on the nature of the investment. While this is largely a matter of judgment, some rules of thumb for annual rates that have arisen over time are 40% for venture capital and 50% for angel investments. Aside from those, there is the risk of being overly conservative in the assessment of relatively straightforward proposals, as well as from conflating financing issues (government grants, refundable tax credits, and pre-approved financing) with operations issues.

- The tax shield arising from the availability of capital cost allowance is well-settled doctrine, whether through the full-year, half-year or other available methods of calculation. Very little work has been done in assessing the calculations under the US MACRS régime, for those Canadian companies that are fully integrated into US operations for tax purposes, but that could be relevant in certain circumstances.

- Equivalent annual cost calculation is a powerful assessment technique that is still little discussed or applied.

- Very little discussion has been given to the different types of capital investment that are undertaken. Som principal categories I have been familiar with include new business, expansion, process improvement, replacement, investment properties, regulatory compliance, and general corporate requirements (eg, head offices, branding, and company-wide IT or communications structures). In any case, different techniques are available for different purposes, and their application should be given detailed discussion.

- Financial reporting under IFRS (but even before that, under the old CICA Handbook) calls for assessment of fair value and impairment of assets under specified conditions. These are important limits that must be considered in any risk analysis for acquisitions.

Updates: Typo corrected; "process improvement" and "investment properties" added in investment categories; give examples of non-relevant financing issues.

09 December 2015

A Body of Knowledge passé?

Several decades back, CMA Canada was doing extensive work in analyzing and compiling best practices for management accounting, and established the CMA Canada Research Foundation to focus on that work. In addition to commissioning various studies, it also issued the Management Accountants Handbook and Management Accounting Practices Handbook for CMAs to abide by. They're quite prominent in my library.

I was recently wondering what is happening to that focus, now that all CMAs, CAs and CGAs are now part of CPA Canada. It turns out that notice was given in 2013 that the Foundation intended to surrender its charter. That has not happened yet, but it appears that it will lapse because of non-continuance under the Canada Not-for-Profit Corporations Act.

That's not all. The Handbooks themselves have never been updated since 1998, although electronic copies of the contents were always available from the CMA Canada website. That site is no longer available, and the new CPA Canada Store does not have access to them.

That's a pity. There was a lot of great advice that came out of this work, and much of the research was seminal in developing management accounting as we know it today. One study in particular, A Practical Approach to the Appraisal of Capital Expenditures, deserves to be updated to cover today's broader range of issues.

I hope CPA Canada revives access to this work. Otherwise, it would appear that our amalgamation was in reality a takeover.

I was recently wondering what is happening to that focus, now that all CMAs, CAs and CGAs are now part of CPA Canada. It turns out that notice was given in 2013 that the Foundation intended to surrender its charter. That has not happened yet, but it appears that it will lapse because of non-continuance under the Canada Not-for-Profit Corporations Act.

That's not all. The Handbooks themselves have never been updated since 1998, although electronic copies of the contents were always available from the CMA Canada website. That site is no longer available, and the new CPA Canada Store does not have access to them.

That's a pity. There was a lot of great advice that came out of this work, and much of the research was seminal in developing management accounting as we know it today. One study in particular, A Practical Approach to the Appraisal of Capital Expenditures, deserves to be updated to cover today's broader range of issues.

I hope CPA Canada revives access to this work. Otherwise, it would appear that our amalgamation was in reality a takeover.

06 November 2015

Better analysis using Gnuplot

My recent posting using images generated from Gnuplot was rather basic. After examining its quite voluminous documentation somewhat cursorily, I have been able to significantly improve the output.

For example, the impact of tax rates and cost of capital on investment in Class 29 assets is illuminated through the use of colour:

Adding a 2D heatmap with the original 3D chart really does clarify the nature of the impact. By specifying different colours to different ranges of after-tax cost, we can more easily gauge the effects.

Adding a 2D heatmap with the original 3D chart really does clarify the nature of the impact. By specifying different colours to different ranges of after-tax cost, we can more easily gauge the effects.

Here it is for Class 53:

You can easily see that the colours are shifting to the left, thus showing that the net after-tax cost is generally becoming cheaper.

You can easily see that the colours are shifting to the left, thus showing that the net after-tax cost is generally becoming cheaper.

And for Class 43:

You can note the impact quite distinctly between the three graphs.I have only just begun to explore this particular application, but I am already impressed with its power.

For example, the impact of tax rates and cost of capital on investment in Class 29 assets is illuminated through the use of colour:

Here it is for Class 53:

And for Class 43:

You can note the impact quite distinctly between the three graphs.I have only just begun to explore this particular application, but I am already impressed with its power.

05 November 2015

A follow-up on the impact of the federal budget

Last spring, I published a post on the impact of changes in capital cost allowance rates on the after-tax cost of investment. I attempted to quantify the impact, but I have wondered since about what would happen if the variables relating to tax rates and cost of capital changed, and how to express that clearly.

I have recently come across gnuplot, an open-source program that helps to chart questions like this, and inputted the data. I decided to plot all possible combinations from 1% to 99% for both cost of capital and composite corporate tax rates.

For the current Class 29 framework, the chart looks like this:

There are two things that immediately stand out:

There are two things that immediately stand out:

Note that this reduces the net after-tax cost attributable to higher costs of capital. This is especially important when such costs are weighted for risk.

Note that this reduces the net after-tax cost attributable to higher costs of capital. This is especially important when such costs are weighted for risk.

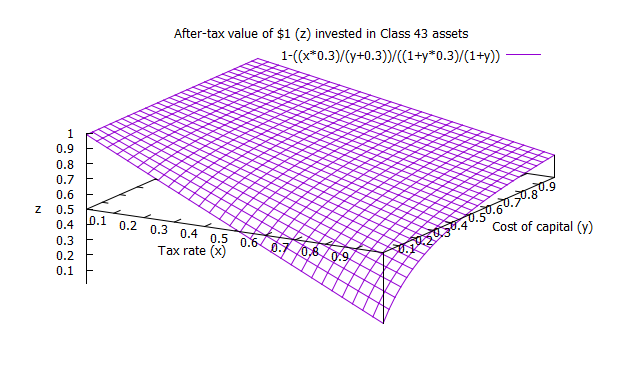

And what about Class 43, which is supposed to return in 2025? While very theoretical, because of the recent change in government in Ottawa, here is what it would look like:

You can see immediately that the cost of capital aberration returns.For that reason alone, I would venture to guess that that option will never return to the Canadian tax structure.

You can see immediately that the cost of capital aberration returns.For that reason alone, I would venture to guess that that option will never return to the Canadian tax structure.

All of these charts do highlight a major flaw in the current system, which all political parties in Canada have failed to see: as lower tax rates make the net after-tax cost of investment much more expensive, that means that current rate reductions given to manufacturing and small business are actually making it more expensive for them to invest in more productive assets. The UK, probably for that very reason, decided recently to abolish its preferential small business rate, and have opted to bring in concepts such as the "patent box" to assign lower tax rates based on the results of specified investments.

That may well be worth implementing here.

I have recently come across gnuplot, an open-source program that helps to chart questions like this, and inputted the data. I decided to plot all possible combinations from 1% to 99% for both cost of capital and composite corporate tax rates.

For the current Class 29 framework, the chart looks like this:

- as the tax rate rises, the net after-tax cost falls; and

- as the cost of capital rises, the net after-tax cost increases as well.

And what about Class 43, which is supposed to return in 2025? While very theoretical, because of the recent change in government in Ottawa, here is what it would look like:

All of these charts do highlight a major flaw in the current system, which all political parties in Canada have failed to see: as lower tax rates make the net after-tax cost of investment much more expensive, that means that current rate reductions given to manufacturing and small business are actually making it more expensive for them to invest in more productive assets. The UK, probably for that very reason, decided recently to abolish its preferential small business rate, and have opted to bring in concepts such as the "patent box" to assign lower tax rates based on the results of specified investments.

That may well be worth implementing here.

Subscribe to:

Posts (Atom)

Why don't Canadian businesses invest?

The tendency of Canadian businesses to under-invest has been noted for decades, and the Fraser Institute reported in 2017 that investment f...