I have recently come across gnuplot, an open-source program that helps to chart questions like this, and inputted the data. I decided to plot all possible combinations from 1% to 99% for both cost of capital and composite corporate tax rates.

For the current Class 29 framework, the chart looks like this:

- as the tax rate rises, the net after-tax cost falls; and

- as the cost of capital rises, the net after-tax cost increases as well.

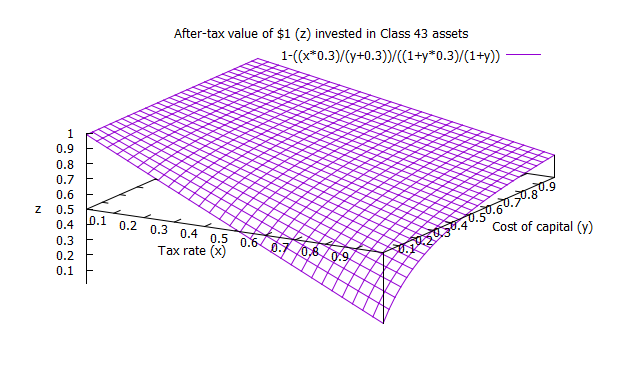

And what about Class 43, which is supposed to return in 2025? While very theoretical, because of the recent change in government in Ottawa, here is what it would look like:

All of these charts do highlight a major flaw in the current system, which all political parties in Canada have failed to see: as lower tax rates make the net after-tax cost of investment much more expensive, that means that current rate reductions given to manufacturing and small business are actually making it more expensive for them to invest in more productive assets. The UK, probably for that very reason, decided recently to abolish its preferential small business rate, and have opted to bring in concepts such as the "patent box" to assign lower tax rates based on the results of specified investments.

That may well be worth implementing here.

No comments:

Post a Comment