- The greater participation of the public sector has called for different types of focus. While the cost of capital will tend towards the risk-free rate, there are also greater requirements for considering optimism bias and sensitivity analysis in different components of proposals, the allocation of risks that arise in public-private partnerships, and consideration of relevant benefits to society (including discussion of what is not relevant).

- In the private sector, more rigorous pre-acquisition analysis is required to determine which components are capital and which are expense, for both financial reporting and tax purposes. This is effectively a 2x2 grid, and there is very little summary literature on the topic.

- In the private sector, the after-tax cost of capital will need to be risk-adjusted depending on the nature of the investment. While this is largely a matter of judgment, some rules of thumb for annual rates that have arisen over time are 40% for venture capital and 50% for angel investments. Aside from those, there is the risk of being overly conservative in the assessment of relatively straightforward proposals, as well as from conflating financing issues (government grants, refundable tax credits, and pre-approved financing) with operations issues.

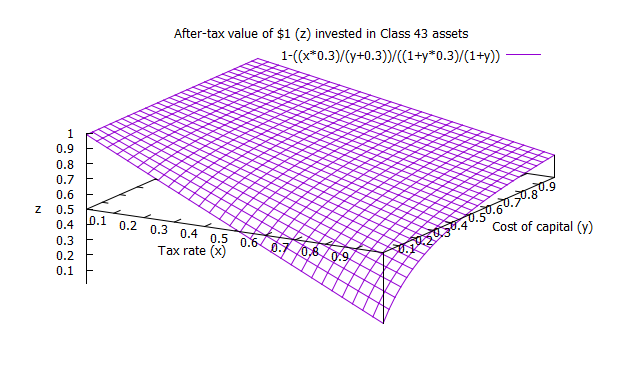

- The tax shield arising from the availability of capital cost allowance is well-settled doctrine, whether through the full-year, half-year or other available methods of calculation. Very little work has been done in assessing the calculations under the US MACRS régime, for those Canadian companies that are fully integrated into US operations for tax purposes, but that could be relevant in certain circumstances.

- Equivalent annual cost calculation is a powerful assessment technique that is still little discussed or applied.

- Very little discussion has been given to the different types of capital investment that are undertaken. Som principal categories I have been familiar with include new business, expansion, process improvement, replacement, investment properties, regulatory compliance, and general corporate requirements (eg, head offices, branding, and company-wide IT or communications structures). In any case, different techniques are available for different purposes, and their application should be given detailed discussion.

- Financial reporting under IFRS (but even before that, under the old CICA Handbook) calls for assessment of fair value and impairment of assets under specified conditions. These are important limits that must be considered in any risk analysis for acquisitions.

Updates: Typo corrected; "process improvement" and "investment properties" added in investment categories; give examples of non-relevant financing issues.